.webp)

There’s a lot of information out there about how to build a startup.

There isn’t so much on how to build a VC firm.

This 4-part series, authored by Jed Ng, founder of AngelSchool.vc , explores the steps involved in launching and running a successful angel syndicate.

- Part 1 - How to Start an Angel Syndicate

- Part 2 - How to Set Up Your Syndicate for Success

- Part 3 - Angel Syndicates: the Deal Process

- Part 4 - How to Build Your Investor Network

Why Start an Angel Syndicate?

Running a syndicate has obvious direct benefits (Carry) and indirect benefits (auto-scaling, deal access and ability to perform diligence). What you might not realise is that these benefits look pretty good even when compared to running a fund:

Let’s delve into carry and auto-scaling in more detail.

Carried Interest

Imagine you invested in a company. It increases in valuation by 11x, generating a 10x profit.

Let's compare two different investment scenarios:

- A direct angel investment of $20,000.

- As a syndicate lead investing $5,000 of your own capital, levering up with $100,000 of syndicate capital and charging 20% carry.

As an angel, your $20,000 investment becomes $220,000. You generate a $200,000 profit on your initial capital or 1000% ROI. Nice.

On the other hand, if you had a syndicate and invested $5,000 of your own money and raised an additional $100,000 through a syndicate:

- Your own $5,000 becomes $55,000, generating $50,000 of profit.

- The $100,000 that your LPs invest becomes $1.1M, with $1M of profit, on which 20% carry generates you $200,000.

By leading a syndicate you've generated $250,000 profit on $5,000 capital at risk, or a 5000% ROI at 4x lower risk.

Venture capital funds work in a similar way. Managers charge a carried interest (generally 20%) across the portfolio of investments.

However, there are some important differences:

Whilst you don’t earn management fees, thanks to deal carry and the lack of hurdles, as a syndicate you actually have a significant mathematical advantage vs. fund models. The difference in upside can be enormous.

This is an argument that some people understand, but you never really see it quantified. Let’s look at a worked example.

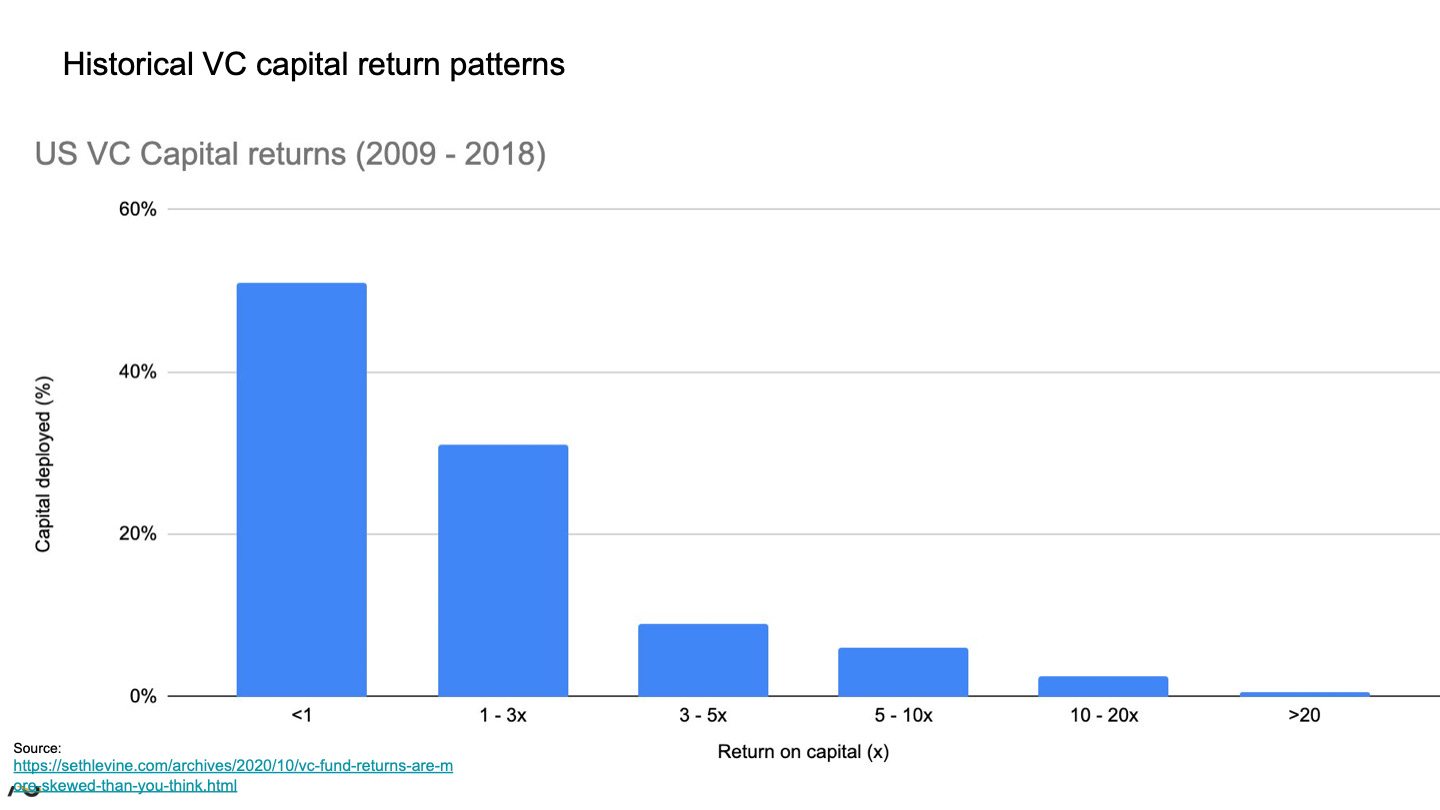

This histogram shows historic VC returns for a 10 year period from 2009 to 2018. As you can see, 51% of funds returned less than 1x capital. That's the first bar. The second bar shows that about 31% returned 1 - 3x. This is where you start to earn carried interest.

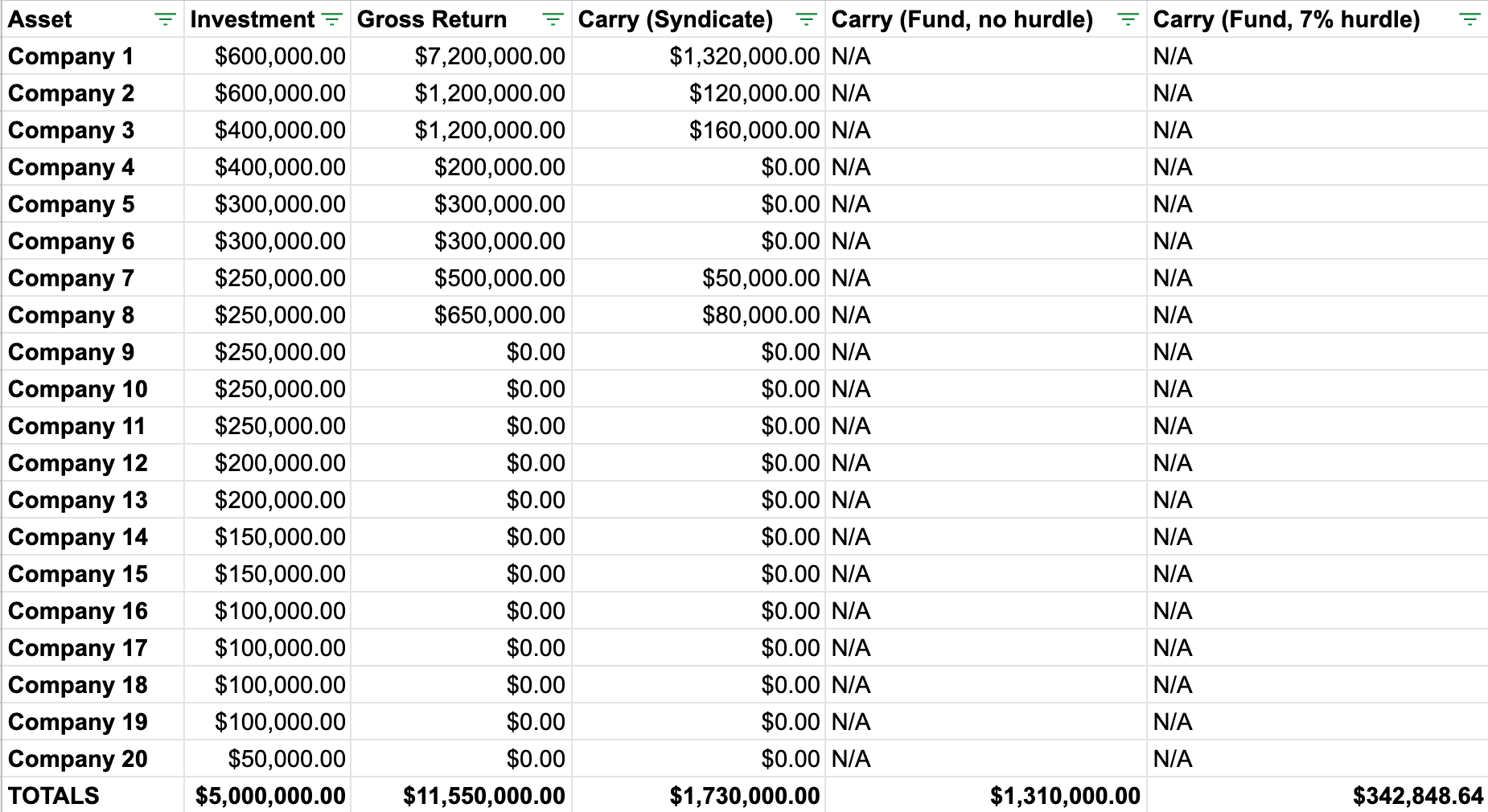

Let's look at the case of two investment firms - an angel syndicate and a fund - that essentially tracked the market. On $5m of capital deployed, assuming average inputs and outcomes, they both invested in ~20 companies and returned ~$11.55m of total capital; i.e. $6.55m of profit.

What did their carry look like?

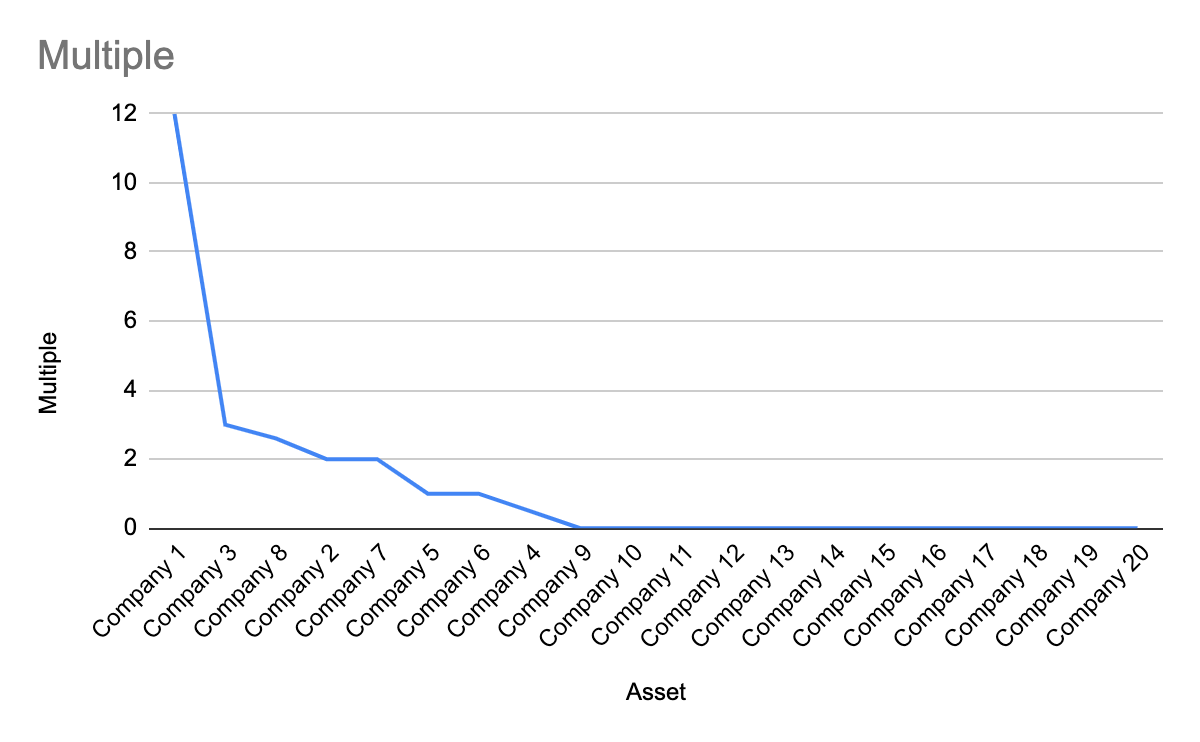

To know the details, we need a sample portfolio - here's one we made one up (you can make a copy and play around with the numbers.

Most portfolios follow a power law distribution, so we have one company responsible for the bulk of the returns, a few that did slightly >1x, and most returning basically nothing.

In the above example, the angel syndicate would earn $1.73m in carry on the $6.55m profit, because they take the carry on every deal individually. The fund, meanwhile, assuming no hurdle rate, would earn $1.31m, because they take their carry on the total profit, not the per deal profit. However, most funds also have a hurdle. Let’s assume 7%, which is fairly standard. Compounded over 10 years (an average fund lifetime), the fund would return just $343k in carry to partners after the hurdle.

So if you see good deals, running an angel syndicate can actually be more profitable than running a fund. It has the added advantage of leaving deal selection to your LP’s, meaning the responsibility for failure sits less squarely with you.

Some people argue (fairly) that syndicates should charge lower carry (10 - 15%) to account for the discrepancy in outcomes. However, 15% - 20% seems to be the market standard for now.

Syndicate “Auto-Scaling”

Syndicates benefit from network effects. This means that as the number of LP’s increases, the utility for the existing LP’s in the syndicate also increases. New LP’s bring more capital, more knowledge (for due diligence) and more deal flow, meaning better quality investment opportunities tend to appear for the group.

If you can figure out how to supercharge referrals, you can boost the rate at which your syndicate grows significantly.

The blue line on this graph shows the number of investors subscribed to my mailing list over time. I’ve overlaid the times when I was active with deal flow.

We see a very clear correlation between deal activity and growth of the investor network. In short, it’s clear that if you can source quality opportunities and run a tight process, you will drive word of mouth and new LP’s will start to sign up.

Most syndicate leads I know, who have seeded their networks the right way, experience the same referral growth loop.

What is this right way?

It’s all about relationships. You are best of starting with your first degree connections. Ultimately people invest in and with people, so your closer contacts are the logical place to start. People who know you and trust you are much more likely to invest with you. If they invest and enjoy the process, they are much more likely to refer people since they already know you.

As word gets out, you can start to build a marketing funnel designed to capture 2nd and 3rd degree connections. The best new members tend to be referrals from your existing network. They are extending your reach via circles of trust.

Imagine this effect compounding and scaling over time as your syndicate grows. It's a really powerful lever.

This is the number one mechanism that we rely on to grow syndicates once we get them going.

Want to know more?

Check out part 2: The Foundations to Set Up Syndicates for Long Term Success.